Over the turbulent past decade, many legacy software players proved to be remarkably resilient. Now they must adopt a new strategic playbook to weather the different challenges ahead.

For the past ten years, the rise of software as a service (SaaS) has reshaped the enterprise-software industry. During that period, the disruptors that pioneered the...

Over the turbulent past decade, many legacy software players proved to be remarkably resilient. Now they must adopt a new strategic playbook to weather the different challenges ahead.

For the past ten years, the rise of software as a service (SaaS) has reshaped the enterprise-software industry. During that period, the disruptors that pioneered the model and the incumbents that transitioned to it created tremendous shareholder value. Between 2011 and 2018, the global software industry’s market cap grew at twice the rate of the overall market. Yet that growth came with a cost: industry profitability tumbled, falling by half over the decade.

The next ten years will not be any less tumultuous. As SaaS matures, the customer’s expectations around ease of use and ease of doing business will continue to rise. Platforms as a service (PaaS) from the Big Three cloud vendors (Amazon Web Services, Google Cloud, and Microsoft Azure) are gaining share and commoditizing software. And with financial markets reeling from the COVID-19 pandemic, investors are looking more closely at bottom-line health.

Addressing these demands will require software vendors to adopt a new playbook. Success will take a renewed strategic focus, a willingness to expand “as-a-service” offerings beyond subscription pricing, and a greater emphasis on profitable growth (see the sidebar, “Software’s new playbook”).

Customers want SaaS products and an SaaS experience

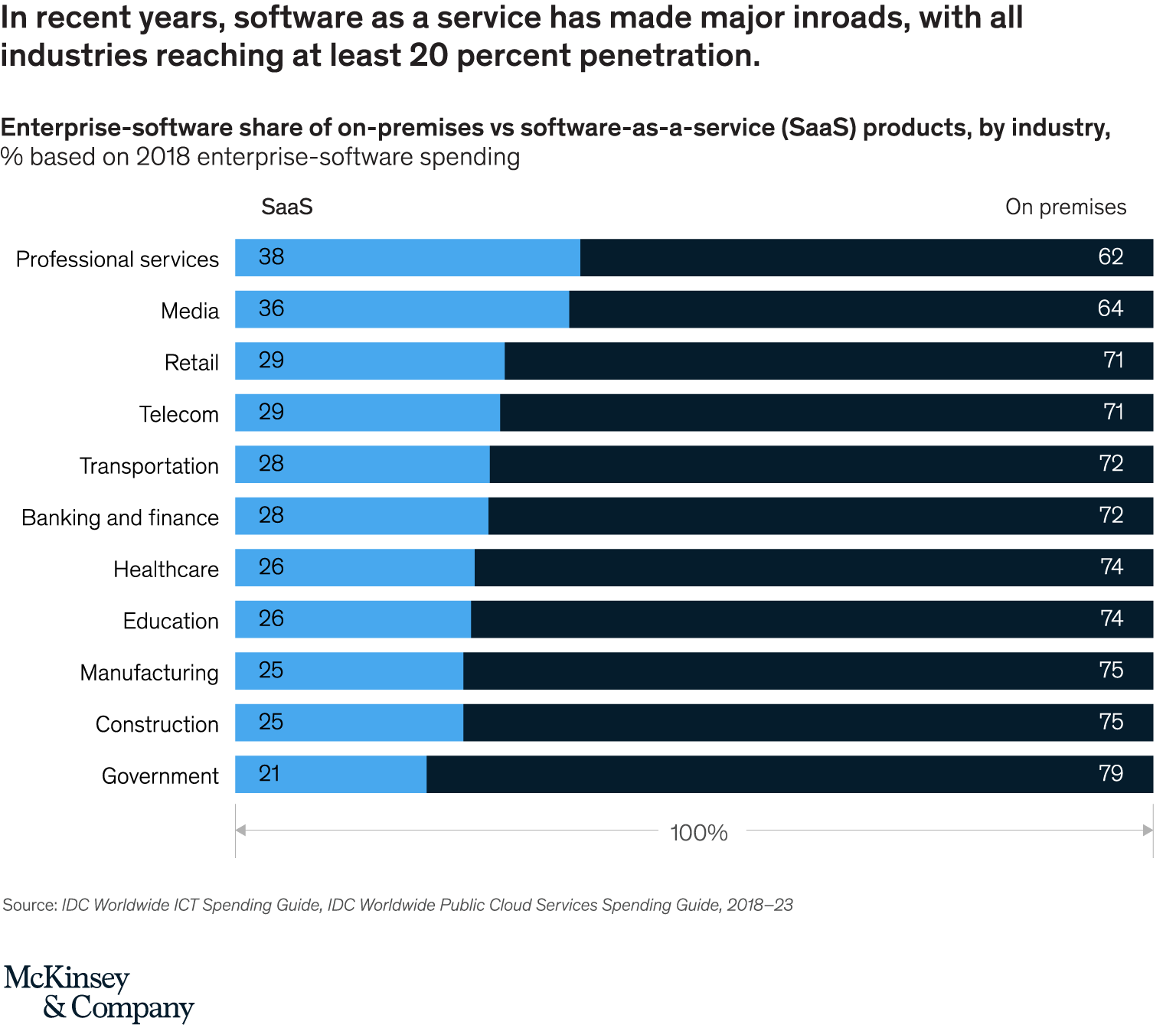

SaaS has become the default software-delivery model—and at breakneck speed (Exhibit 1). In 2010, SaaS offerings commanded just 6 percent of enterprise-software revenues. By 2018, that share had grown to 29 percent, or $150 billion globally. Yet that figure understates the true size of the market. When revenues from companies still transitioning to SaaS are counted, the total as-a-service share rises to 75 percent of all enterprise-software revenues, or more than $380 billion. Those numbers mean that companies with no SaaS offerings now represent only one-quarter of total industry revenues.

In a sign of the market’s maturity, late adopters have come on board. More than one-fifth of all government software spending now goes to SaaS. Even categories such as CAD, whose highly expert customer base would normally resist sweeping product changes, are making the transition.

Vendors that have not yet begun their SaaS transformation must do so now. The “next normal” established during the COVID-19 pandemic will accelerate the footprint of SaaS, given the growth of remote working, the rapid deployment of digital solutions, and the lower up-front costs.

To succeed with SaaS, however, vendors must do more than offer a subscription-pricing model on a product hosted in the cloud. They need to match the streamlined, customer-friendly as-a-service product-delivery experience with a similarly streamlined and customer-friendly end-to-end journey. Right now, the customer experience of many SaaS vendors often feels disjointed. All too frequently, for instance, legacy billing processes and order forms riddled with confusing product terminology make it hard for customers to know what they’re paying for. Leading players address these inconsistencies by evaluating the whole business in the as-a-service context and redesigning core processes to make them more intuitive and responsive.

Source - mckinsey

#nextgenerationSAAS #collaboration #systeminfrastructure